Workers Compensation

The Knock You Really Don't Want: Florida's Workers' Comp "2x Penalty" — What It Means for Your Business

Most contractors figure they're ready for an insurance audit. What they're not ready for? A state investigator walking onto their job site.

The Visit Nobody Sees Coming

Picture this. Tuesday morning. Crew's working, drywall's going up, and for once — miracle of miracles — the project is actually on schedule.

Then two people show up with clipboards and badges. Not from your insurance company. Not OSHA either.

They're from the Florida Department of Financial Services, Bureau of Compliance. (Yeah, it's a mouthful.) These are sworn state investigators. They carry badges. They've got subpoena power. And they absolutely do not need a warrant to walk onto your job site and start asking questions.

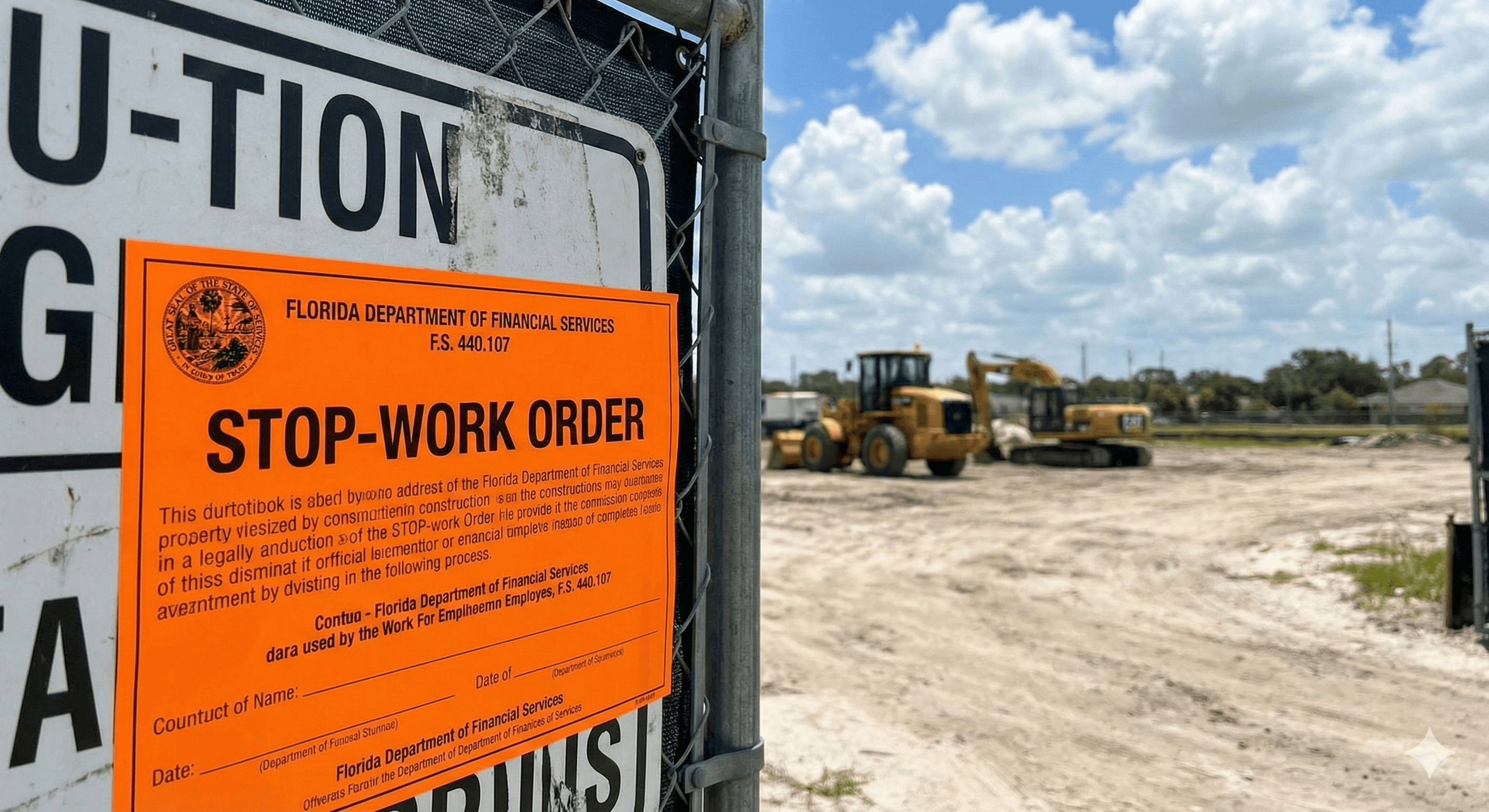

If they find someone on site without workers' comp coverage — or without a valid exemption — they can issue a Stop-Work Order right then and there. Hammers down. Site goes quiet. And then comes a penalty that'll make your annual insurance audit look like pocket change.

I'm not trying to scare you here. This is just how it works under Florida Statute § 440.107. And it catches contractors who genuinely thought they had everything squared away.

Part 1: What Does the Law Actually Say?

Let's get specific.

F.S. 440.107 gives the state authority to enforce workers' comp coverage across Florida. Here's what the Department of Financial Services is allowed to do:

- Show up at your job site unannounced. No warning, no appointment.

- Verify coverage for everyone on site — your guys and your subs' guys.

- Issue a Stop-Work Order if they find non-compliance.

- Hit you with a penalty up to double the premium you should have paid.

- In serious cases? Refer you for criminal prosecution.

This isn't your carrier calling to true up your payroll estimate. This is state law enforcement with the authority to shut your project down.

The Part That Keeps GCs Up at Night: F.S. 440.10(1)(b)

Here's where things get uncomfortable.

Under F.S. 440.10(1)(b), if your subcontractor doesn't have valid workers' comp coverage (or a valid exemption), their employees get treated as YOUR employees. For workers' comp purposes, anyway.

Think about what that means. The second an uninsured sub steps onto your job, Florida law considers their workers to be on YOUR payroll. You become what's called the "statutory employer." Which means you owed premium on those workers. And if you didn't pay it — because you had no idea the sub's coverage had lapsed — the state might view that as misrepresentation of payroll.

That's not an administrative hiccup. That's the trigger for penalties.

Part 2: The Math — It's Not What Most People Think

This is where the rumor mill does real damage.

The Myth Everyone Believes

I hear it constantly: "If I paid an uninsured sub $100,000, I'll get hit with $200,000 in fines."

Nope. That's not how this works.

The penalty under F.S. 440.107 is calculated as double the avoided premium — not double the wages. Sounds like good news at first. But the way "avoided premium" gets calculated? It can actually produce fines higher than the "double wages" myth would suggest.

The Actual Formula

Section 440.107(7)(d)(1) lays it out:

Avoided Premium = (Payroll ÷ 100) × Class Code Rate

Penalty = Avoided Premium × 2

Payroll = gross wages during the non-compliance period.

Class Code Rate = the rate assigned to the type of work being done. And this is where it gets ugly, because rates vary wildly depending on the trade.

Why Class Codes Matter More Than You'd Think

The penalty tracks to premium, which tracks to risk. Higher-risk work means higher rates means bigger penalties.

Example A: Low-Risk Work (Office Staff)

A call center fails to cover its clerical employees.

Component

Value

Payroll

$100,000

Class Code

8810 (Clerical)

Rate

~$0.13 per $100

Avoided Premium

$130

2x Penalty

$260

Minimum penalty kicks in: $1,000. Not great, but survivable.

Example B: High-Risk Work (Roofing)

A roofing contractor pays his crew cash, no records.

Component

Value

Payroll

$100,000

Class Code

5551 (Roofing)

Rate

~$8.25 per $100

Avoided Premium

$8,250

2x Penalty

$16,500

That's over 16% of the gross payroll. On top of the Stop-Work Order.

Rate Reference (Approximate 2025 Numbers)

Trade

Rate per $100

Penalty on $100K Payroll

Office/Clerical

$0.13–$0.50

A few hundred bucks

Plumbing

$2.50–$4.00

$5,000–$8,000

Electrical

$3.00–$5.00

$6,000–$10,000

Carpentry

$6.00–$10.00

$12,000–$20,000

Concrete/Masonry

$8.00–$12.00

$16,000–$24,000

Roofing

$8.00–$10.00

$16,000–$20,000

Tree Work/Landscaping

Varies ($6.00+)

Depends on scope

That roofing sub you've used on a bunch of jobs? If they're not covered, the penalty alone could exceed the contract value.

Part 3: Imputed Payroll — Where the Real Nightmares Come From

If the standard penalty is a precision strike, imputed payroll is carpet bombing.

This is how you end up with fines that seem completely disconnected from reality.

What Triggers It

The "2x Premium" formula needs actual payroll numbers to work. But construction is full of cash payments, off-the-books labor, and — let's be honest — lousy record-keeping.

So the legislature gave the DFS a tool: F.S. 440.107(7)(e). If you can't provide records sufficient to determine actual payroll, the state gets to impute it.

Translation: if you can't prove what you paid, they make up a number. And it won't be in your favor.

How the Math Works

When payroll is imputed, the DFS doesn't use minimum wage as the baseline. They use something much less friendly:

Imputed Wage = 1.5 × Statewide Average Weekly Wage (SAWW)

For 2025, the SAWW runs about $1,295 per week. So:

- Imputed weekly wage: $1,295 × 1.5 = $1,942.50

- Annualized: $1,942.50 × 52 = $101,010 per employee per year

The "No Records" Horror Story

Small contractor hires two day laborers for one week to help on a rush job. Pays them $500 each in cash. Total: $1,000. No records because, hey, no paper trail means no trail to follow. Right?

Investigator spots the workers. Contractor can't prove they only worked one week.

What the DFS assumes: Both workers were employed full-time for the entire 2-year look-back period.

What Actually Happened

What the State Calculates

Wages paid: $1,000

Imputed payroll: $404,040

Premium: $33,333

Penalty: $66,666

Effective penalty rate: 6,666% of actual wages paid.

This is why the "double the wages" myth is dangerous. It understates the risk. Even with rates at historic lows, the imputed payroll mechanism can still generate a penalty that destroys a small contractor. For someone with poor records, the penalty isn't double anything — it's whatever arbitrary number the statute produces. And that number can kill a business.

Part 4: The Look-Back Period

The DFS doesn't just look at the day they caught you. Under the statute, they can audit payroll records going back 24 months from the Stop-Work Order date.

- Operating without coverage for five years? Penalty capped at the last two.

- Business only existed for six months? Penalty covers those six months.

- Used a sub whose exemption expired 18 months ago across three projects? Potential penalty on all three.

Important: the burden falls on YOU to prove when you started operations or when you last had coverage. No records? They assume the maximum look-back applies.

Part 5: The 15% Tutorial Discount (This Is Real)

Here's something most people don't know about.

F.S. 440.107(7)(d)(1)c created a provision for employers who haven't received a Stop-Work Order before. If you complete an online workers' comp compliance course, you can get 15% knocked off your final penalty.

The catch:

- You need to score at least 80% on the quiz.

- You have to complete it within 21 days of the records request.

It's a real opportunity to cushion the financial hit. But most employers miss the deadline because they're in full panic mode dealing with the shutdown. If you ever find yourself in this situation, put the tutorial on your calendar immediately.

Part 6: How Investigations Get Started

Who Shows Up

The DFS Bureau of Compliance employs investigators with actual police powers. Badges. Subpoena authority. No warrant required to enter your job site.

They often wear state-issued hard hats and vests. But don't confuse them with OSHA safety inspectors. They're law enforcement.

Before they announce themselves, investigators typically scope the site from a distance. Count heads, document what tasks are happening, note what equipment is in use. That way, when you later claim the ten guys on the roof were just "friends stopping by," it doesn't hold up.

Their main weapon is the on-site interview. They're trained to separate workers from supervisors immediately — before anyone can coordinate a story. The questions are designed to demolish the "independent contractor" defense:

- "Who picks you up in the morning?"

- "Do you bring your own ladder?"

- "Who tells you what to do each day?"

- "Do you work for anyone else?"

If a worker admits to being paid cash, picked up by the boss, and given direct instructions? The independent contractor argument just evaporated.

What Triggers an Investigation

Random sweeps. Investigators drive around looking for active sites — residential remodels, roofing jobs, new construction. They check permits, walk on site, start checking IDs. No warning whatsoever.

The state is aggressive about this. In the 2022-23 fiscal year, the Bureau of Compliance issued over 1,900 enforcement actions. And it's not just civil penalties. Sting operations in Tampa and Miami during 2024 led to more than 20 felony arrests for workers' comp fraud and unlicensed contracting.

Tip line calls. Florida has a workers' comp complaint line. Calls come from subs who didn't get paid and want revenge, competitors who want you off a bid, workers who got hurt and discovered there was no coverage, or just anonymous tipsters.

Database cross-referencing. The DFS matches building permits against workers' comp policy data. Pull a permit for a $500,000 job but your reported payroll doesn't add up? You might get flagged.

Injury reports. If someone gets hurt on your site and files a claim, the state often investigates. If that worker belonged to an uninsured sub, the investigation may expand to include you as the statutory employer.

What Happens When They Arrive

Typical sequence:

Investigators show up unannounced, identify themselves.

Request a list of everyone on site.

Check each person against the state's workers' comp database.

Verify that any exemptions are current.

May call carriers directly to confirm active coverage.

If anyone is uninsured and not exempt → Stop-Work Order.

Request payroll records to calculate the penalty.

Work stays stopped until you pay up and prove compliance.

Part 7: What a Stop-Work Order Actually Means

This is the nuclear option.

The Legal Basis

F.S. 440.107(1) declares that failing to comply with workers' comp requirements creates "immediate danger to public health, safety, and welfare." That language authorizes ex parte action — meaning they shut you down first, hearing comes later.

It's Not Just the One Site

Common misconception: the Stop-Work Order only affects the site where the violation happened.

Wrong.

The order is issued against your entity, not a location. If a plumbing contractor has crews working ten different jobs across three counties, and an investigator catches a problem at one site, the SWO shuts down:

- That site

- The other nine sites

- The corporate office

- Everything

Your entire revenue stream gets cut off instantly.

Working in Violation Is a Felony

The SWO isn't a suggestion. F.S. 440.105 makes it a third-degree felony to work in violation of a Stop-Work Order. Plus there's a civil penalty of $1,000 per day for every day you operate in defiance.

Getting the Order Released

Your business stays frozen until you meet the state's conditions:

Get insured. Obtain a valid workers' comp policy and prove it to DFS.

Pay something now. Minimum $1,000 down toward the assessed penalty.

Agree to a payment plan. Sign a Periodic Payment Agreement for the balance.

This puts employers in a terrible negotiating position. To get cash flowing again, you have to agree to the state's terms — often before you fully understand how big the penalty actually is.

Part 8: Stop-Work Order vs. Annual Audit — Not the Same Thing

Contractors mix these up constantly. They're completely different animals.

Carrier Audit

State Investigation

Who

Your insurance company

DFS Bureau of Compliance

When

Policy renewal time

Any time, unannounced

Purpose

True up your premium

Law enforcement

Result

Pay the difference (1x)

Pay 2x penalty + fines

Work impact

None

Stop-Work Order

Criminal risk

None

Possible felony charges

Your carrier audit is accounting. A state investigation is law enforcement.

Part 9: The Statutory Employer Problem

Being the direct employer doesn't get you off the hook. The Statutory Employer Doctrine can reach up and grab you.

F.S. 440.10(1)(b) says that when you sublet work to a subcontractor, you're both considered part of the same business. You're liable for workers' comp payments if the sub isn't covered.

How It Plays Out

When a sub gets hit with an SWO, here's what happens to you:

Project stops. The sub can't work, so your project stalls.

Financial exposure. If an employee of the uninsured sub gets hurt, they can file against YOUR policy. You're the statutory employer. Medical bills land on you.

Audit surprise. When your annual audit rolls around, the carrier will charge you premium for that sub's labor — at your rates. That can be a massive unexpected bill.

Part 10: The Exemption Trap

The exemption system looks like a loophole. In practice, it's a minefield.

Construction vs. Non-Construction Rules

Construction:

- Only 3 officers (or LLC members) can be exempt

- Must own at least 10% of the company

- Costs $50 per exemption

- Only covers the specific individual named

Non-Construction:

- No limit on exempt officers

- Free to file

The "Helper" Problem

Classic scenario: Owner-operator gets an exemption for himself. Hires a "helper" to hand him tools. Thinks the exemption covers everything.

It doesn't. The moment that helper steps on site, the business has an employee. No policy means non-compliance. SWO gets issued.

Exemptions Can Disappear

They expire every two years. And the exempt individual can revoke at any time.

A sub might give you a valid exemption certificate in January. Come March, they revoke it — maybe to sue for benefits after an injury, maybe it just lapses. If you're not checking the state database regularly, you have no idea. And you're exposed.

Part 11: The Audit Process — Worse Than Taxes

Once the Stop-Work Order hits, an audit kicks in that makes your tax prep look like a walk in the park. You get a Request for Production of Business Records (form DFS-F4-1595) and a 10-business-day deadline to produce everything.

What They Want

- Federal tax returns (1040, 1120, 940, 941)

- State tax forms (UCT-6)

- Bank statements for all business accounts

- Check registers with front and back images

- General ledgers and cash disbursement journals

- Contracts and invoices — both upstream and downstream

What Auditors Look For

These people are forensic accountants. They know the tricks.

Check cashing patterns. Recurring checks made out to "Cash" or to the owner personally? They'll assume it's net payroll for a crew and gross it up.

"Materials" payments. Paid a sub $2,000 for "materials" but there's no receipt? Gets reclassified as wages.

Digital transfers. Venmo or Zelle payments to someone named "Jose" or "Mike"? Flagged as unreported payroll.

Class Code Games

Auditors also watch for misclassified codes. If you put workers down as "Janitorial" or "Drivers" but can't document exactly how many hours they spent on each task, the auditor applies the highest-rated code to everything.

Worker spent 1 hour roofing and 39 hours driving, but you can't prove the split? All 40 hours get classified as roofing. Penalty just jumped 10x or 20x.

Part 12: The Independent Contractor Myth

Biggest source of non-compliance I see: people relying on "independent contractor" status to avoid coverage requirements.

The 10-Factor Test

Florida uses a detailed test to determine whether someone is actually an employee. Key factors:

- Control: Is the boss directing the details? ("Put that shingle there.")

- Tools: Does the boss provide equipment?

- Supervision: Is the work being supervised?

- Payment structure: Hourly or by the job?

If someone gets paid by the hour, shows up when they're told, and uses the boss's equipment, they're probably an employee. Doesn't matter what the contract says.

Construction Is Even Stricter

F.S. 440.02(15)(c)(3) essentially requires that any sub who isn't a separate business entity with their own workers' comp exemption or policy... is your employee.

The 1099 Trap

Slapping a 1099-NEC on someone at year-end doesn't protect you. When auditors show up, that stack of 1099s looks like a confession — a helpful list of uninsured employees you documented yourself.

Part 13: The Database Lag Problem

Even if you verify coverage, you might still get burned.

The Issue

The DFS Proof of Coverage database doesn't update in real-time. Carriers have up to 21 days to report policy changes. Then the state needs time to process the info.

So a sub's policy could get cancelled on the 1st, but the database might show "Active" until the 25th. If that sub walks onto your job on the 15th, you just hired an uninsured contractor. And the database told you everything was fine.

What This Means

A Certificate of Insurance is a snapshot from one moment. It doesn't tell you coverage exists today. To actually verify:

- Call the agent or carrier on the COI

- Confirm the policy is currently active

- Ask about pending cancellations

- Document the call — date, time, who you spoke with

Part 14: What Real Compliance Actually Requires

If you want to be bulletproof, here's the workload:

Daily exemption checks. Log into the state database before every shift to make sure no sub has revoked.

Monthly carrier verification. Call the agent for every sub to confirm policies haven't lapsed.

Policy exclusion review. Get the actual declarations pages and confirm the policy covers the work being done.

Document everything. Screenshots, call logs, COIs — all of it. "I thought he was covered" won't hold up.

The reality? Nobody can do this manually for 20+ subs. That's why GCs get fined. Not because they're trying to cut corners, but because the compliance standard is basically impossible without some kind of system.

Part 15: The Stakes

Scenario

Potential Exposure

One uninsured roofing sub ($100K payroll)

$16,000–$20,000+ penalty

Three uninsured subs over 2 years

$50,000–$100,000+

Missing records / Imputed payroll

$101,000+ per employee penalty basis

Stop-Work Order on $500K project

Lost revenue, delay damages, idle crew

Name on public violator list

Reputation damage, bonding issues, carrier problems

Injury to uninsured sub's employee

Claim hits YOUR experience mod; premiums spike for years

For a lot of contractors, this isn't "cost of doing business." It's a business-ending event.

So What Do You Do?

You can't predict when the state shows up. But you can control what they find.

Ask yourself:

- Do I know — right now, today — that every sub on my site is covered?

- Could I produce documentation proving I actually verified?

- If an exemption expired last month, would I know about it?

- If a policy got cancelled for non-payment, would I find out before an investigator does?

If you're not confident on any of those... you've got a gap.

The state doesn't demand perfection. But they expect a system — documentation, verification, a process that shows you're actually trying. Building that system manually is nearly impossible once you're past a handful of subs.

Figure out what works for your operation. Dedicated admin person. Compliance service. Software tool. Something. But figure it out before someone else figures it out for you.

This article provides general information about Florida Workers' Compensation enforcement under F.S. 440.107 and related statutes. It is not legal advice. Penalty calculations, class code rates, and enforcement practices vary based on circumstances and change over time. Consult a qualified attorney or licensed insurance professional for guidance specific to your situation.